》Check SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View Historical Prices of SMM Metal Spot Cargo

SMM, February 24, 2025:

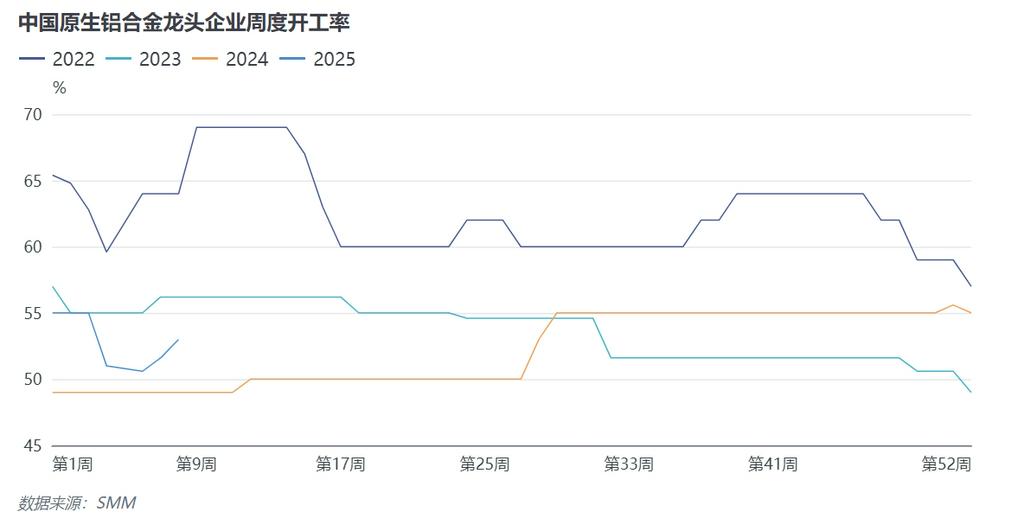

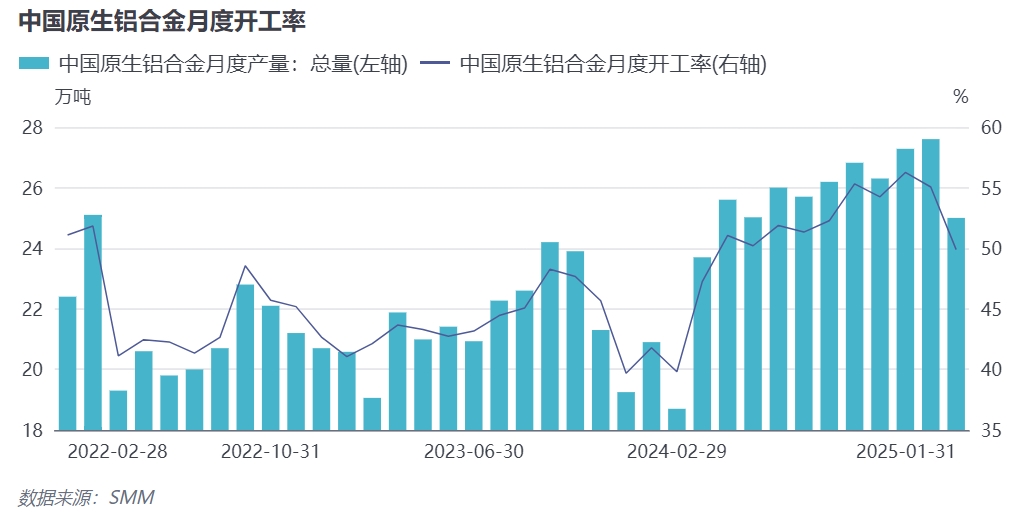

According to the SMM survey, the operating rate of China's primary aluminum alloy industry in January was 49.88%, down 5.17 percentage points MoM, with a significant decline due to the Chinese New Year holiday. Based on the SMM survey, during the last week before the Chinese New Year, although more than half of the enterprises had no plans to adjust production, it was expected that normal production would continue during the holiday. Some enterprises reported that they were still fully engaged in taking orders and production, with little to no impact on their operating rates. However, some enterprises chose to slow down production, and northern customers indicated that the operating rate in January might drop by 10-20% compared to normal levels. Additionally, some enterprises utilized the holiday period for shutdowns and maintenance, leading to an overall weakening of the operating rate for primary aluminum alloy as the holiday approached. During the Chinese New Year holiday, some enterprises further reduced liquid aluminum output, with expectations for production cuts during the holiday. Leading enterprises in the industry experienced varying degrees of decline in operating rates.

January and February are traditionally the off-season for primary aluminum alloy. Although orders before and after the holiday were less than ideal, enterprises showed a slightly higher willingness to produce primary aluminum alloy compared to aluminum billet, driven by the need to complete liquid aluminum alloying tasks and considerations of profitability, efficiency, supply, and demand. The operating rate of the primary aluminum alloy industry in January was slightly higher than previously expected. According to the SMM survey, as more than half of the enterprises maintained normal production during the holiday, the operating performance in the first week after the holiday showed little difference from the last week before the holiday. Some enterprises even experienced a slight increase in operating rates after the holiday, performing relatively well. However, February as a whole remained an off-season for the primary aluminum alloy sector, with some producers adopting a wait-and-see approach and maintaining a slow production pace. In mid-to-late February, as downstream sectors of primary aluminum alloy resumed operations after the holiday, demand was expected to improve, and the operating rate of primary aluminum alloy might recover to levels close to normal before the holiday. SMM expects the operating rate of China's primary aluminum alloy industry in February to recover to around 53%.

Will demand "accelerate" after the Lantern Festival? How many hurdles remain for primary aluminum alloy enterprises this spring? SMM provides the following analysis of operating rates over the past three weeks after the holiday:

1. Operating Rates Rebounded Weekly, but Recovery Was Gradual

-

Changes in Operating Rates Over Three Weeks After the Holiday : Gradually increased from 50.6% in the week of February 6 to 53.0% in the week of February 20, up 2.4 percentage points cumulatively, showing a slight stepwise recovery.

-

Driving Factors : Downstream enterprises gradually resumed work after the holiday (e.g., some regions resumed on the eighth day of the lunar calendar, while others returned after the Lantern Festival), leading to marginal improvements in demand.

-

Restraining Factors : February's traditional off-season, combined with rising aluminum prices, suppressed demand release. Overall production remained conservative, with no explosive growth observed.

2. Significant Structural Divergence in the Market

-

Differences in Enterprise Performance : A few enterprises increased production due to improved orders, but most reported demand lagging behind supply , characterized by:

-

increased production but shipments falling short of expectations, resulting in a short-term supply-demand mismatch;

-

rising aluminum prices (cost pressure) leading to cautious downstream procurement, suppressing demand elasticity.

-

3. Off-Season Characteristics Remain Dominant

-

Producers maintained a strong wait-and-see sentiment, with some operating at low capacity;

-

downstream resumption progress was slow, and actual demand recovery was weaker than expected, dragging down the pace of operating rate recovery.

4. Future Outlook: Gradual Recovery to Continue

-

Positive Signals : Downstream operating rates continued to rebound after the Lantern Festival, with demand expected to further improve;

-

Potential Pressures : High aluminum prices may continue to suppress restocking enthusiasm, limiting the upside room for operating rates;

-

Expected Path : In the short term, operating rates may continue a mild upward trend, but attention should be paid to aluminum price trends and the actual recovery of end-use demand (e.g., in automotive and construction sectors).

Summary : The current primary aluminum alloy market is in a "weak recovery during the off-season" phase, with a slow and uneven pace of demand recovery. The industry as a whole awaits the arrival of the peak season (after March) to confirm substantial improvement. Enterprises need to strike a balance between inventory control and flexible production adjustments.